Credo CEO Interview: The Most Important Thing From Earnings

Last time I was bullish on Credo, the stock doubled in four months. I'm bullish again.

Credo is crushing it.

In February, Credo pre-announced an incredible revenue range for its fiscal third quarter of $404 million to $408 million versus the prior guidance range of $335 million to $345 million. On Monday, the company gave the finalized revenue figure of $407 million, up 202% year-over-year and 52% quarter-over-quarter.

Credo is a leader in high-speed data connections for AI data centers. The company pioneered active electrical cables, or AECs, which are copper-based cables that connect AI hardware infrastructure together. They are more reliable and consume less power than optical cables and can reach longer distances than traditional passive copper cables. AECs are the largest part of Credo’s business, but the company is also expanding into optical connectivity solutions.

Source: Credo

“With continued growth in AECs and ICs and the announcement of three new multi-billion dollar TAM expansions through ZeroFlap optics, ALCs, and OmniConnect, we remain confident in our ability to innovate and grow in the expanding AI infrastructure landscape,” Credo CEO Bill Brennan said in the earnings release.

Key Context spoke with Brennan late Monday after the analyst conference call to discuss what hyperscaler customers are saying, the competition in the AEC and optical space, and what Nvidia’s upcoming AI GPUs mean for the company.

Tae’s Take on Credo stock follows the Q&A.

Here are edited highlights from our conversation with Brennan:

Key Context: I saw Credo acquired CoMira Solutions. I assume it is a small deal?

Brennan: It was what you would consider to be financially more of a tuck-in. We didn’t need to announce the deal. But strategically for us, it’s pretty important. We had been partnered with CoMira for four years. They have a strong team and reputation for protocol IP and error correction. We collaborated well with them. We’re bringing on the order of 15 highly skilled engineers to our team.

For Credo’s major hyperscaler customers, I assume you are talking to them and you have visibility on how they’re building data centers over next few quarters?

Absolutely. Over the next year. And for a couple customers, I actually get two years of visibility.

The simple bear story out there is that there’s going to be an AEC to co-packaged optics transition. But Credo has argued AEC is going to be complementary and it is still early for AECs, walk through that for us.

If we think today about where our customer base is and where the market is generally, there has not been a full transition to 100 gig per lane. We’re still seeing a transition into 100 gig per lane. By the way, 100 gig per lane, we’re going to sell our entire portfolio, including AECs. It’s going to be the largest part of our revenue base. But you’re also going to see ZeroFlap optics. We’ll have an inflection point in fiscal 2027.

[Editor’s note: Credo said on the call its ZeroFlap optics business will have a strong ramp in first quarter fiscal 2027 which is faster than they believed three months ago]

We’re seeing tremendous interest in the product because we’re delivering best-in-class reliability. We talked about the effect of link flaps, these intermittent failures. That can bring an entire cluster down. That’s been first and foremost with our customers and their mindset about solutions that they want to source. We’re the first solution in the optical space.

Let’s talk about next generation, which is 200 gig per lane, and those are really 1.6T ports. The way that the market looks right now, it looks that the ecosystem will stay the same. We’ll do very well with AECs. We’ll do very well with ZF optics.

CPO [Co-packaged optics] has been a conversation since December, and this is really for the 400 gig scale up. You’re still going to have issues with reliability. In scale up, reliability is going to be just as important as scale out because there’s no redundancy between the GPU and the switch within that network. And so if you compared pluggable optics, you’ve got reliability issues. When you’ve got a CPO with a thousand lasers and it’s highly integrated, the industry still hasn’t answered the question about the serviceability of or the maintainability of the solution. And when if you listen to the marketing machine from some of these big players, they would tell you that two hundred gig is already over. We haven’t even ramped any two hundred gig yet.

We rely on others to do the high-level market forecasting [on CPO]. And the one that was referenced to me was low single digits for the next three years. I’m talking about a small percentage. And then, people are making doomsday predictions about the end of copper.

What’s the current competitive threat from rivals like Marvell in the AEC space?

For AECs, we’ve had pretty strong competition for the last four years. And the reason that we still have maintained such a high market share is because our approach to the market is fundamentally different. We’re a system level solution provider. We take ownership of the entire solution. From SerDes to ICs to AEC Design. And qualification to supply chain management to customer go-to-market. It’s all under one roof. And our ability to respond more quickly and in a way that delivers more predictably to our customers. That’s why we’re maintaining our market share. Everybody else, I can’t even imagine the anxiety that I would have selling a chip to another company and hoping they took it the additional ninety-nine yards that they would need to take.

What’s the biggest takeaway from the earnings report?

In the earlier call, we had indicated that we expected a ramp in second half of our fiscal 2027 [for ZeroFlap Optics]. And so, for us to be able to confirm that it’s going to start in first quarter, that’s pretty big news. It’s gone through the same rigor that our AECs have gone through.

We’ve already started production with one customer that we announced. But we’ve got three others in qualification right now. So that’s probably the number one takeaway from the call is that we’re going to see a material amount of revenue in fiscal 2027 from this brand new product.

What is the impact on Credo’s business as Nvidia’s Vera Rubin hits the market versus Blackwell Ultra? Does it change anything?

Faster is better. More connections are better. If you look at the largest volume of the connections that we’re making right now, it’s with Nvidia gear. We had some great demos at OCP [conference] showing how elegant the AECs will fit within those architectures for the scale-out part of that network.

Thanks for your time, Bill.

Source: CNBC

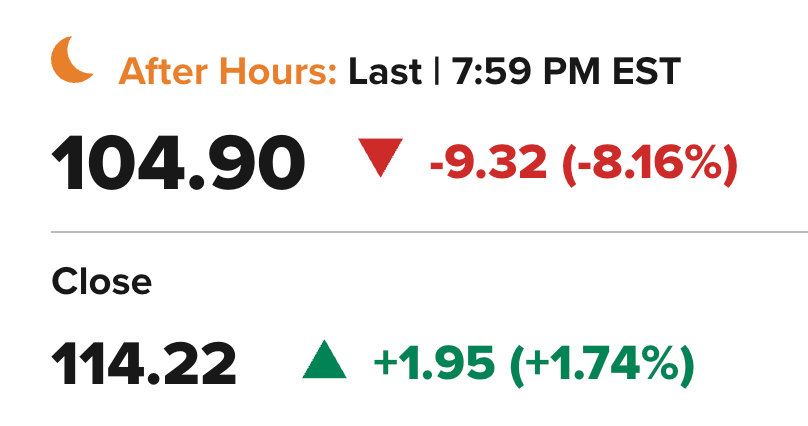

Tae’s Take: After the conference call with analysts, Credo stock was down 8.2% to $104.90 in after-hours trading. The only disappointing element I can point to was the gross margin guidance of 64% to 66% for the current quarter, versus 68.6% in the third quarter.

Management on the call said the margin guidance was “conservative.” They gave the same outlook range for the third quarter three months ago. I believe they are being conservative, as they were last time.

I would focus on Brennan’s positive comments on hyperscaler visibility and the new ZeroFlap optics business, which is ramping faster than expected. I also believe AECs will be a more durable business than the skeptics suggest, and the transition to optical will not be abrupt but rather complementary at first.

The last time I was bullish on Credo, the stock doubled in four months. I’m bullish again.